GUEST BLOG / By Mona Mahajan and Greg Fehr, Edward Jones Company--Markets react to a full-scale invasion by Russia. Equity markets moved sharply lower yesterday morning around the globe, with U.S. indices adding to losses and European markets lower by 3.0% - 4.0%.1.

These moves come as Russian President Putin began a full-scale invasion of Ukraine last night, violating international law and inciting acts of war. In response, oil prices have also moved higher, with WTI crude briefly surpassing $100, and investors have flocked to traditional safe-haven assets, including U.S. Treasury bonds, the U.S. dollar, and gold.

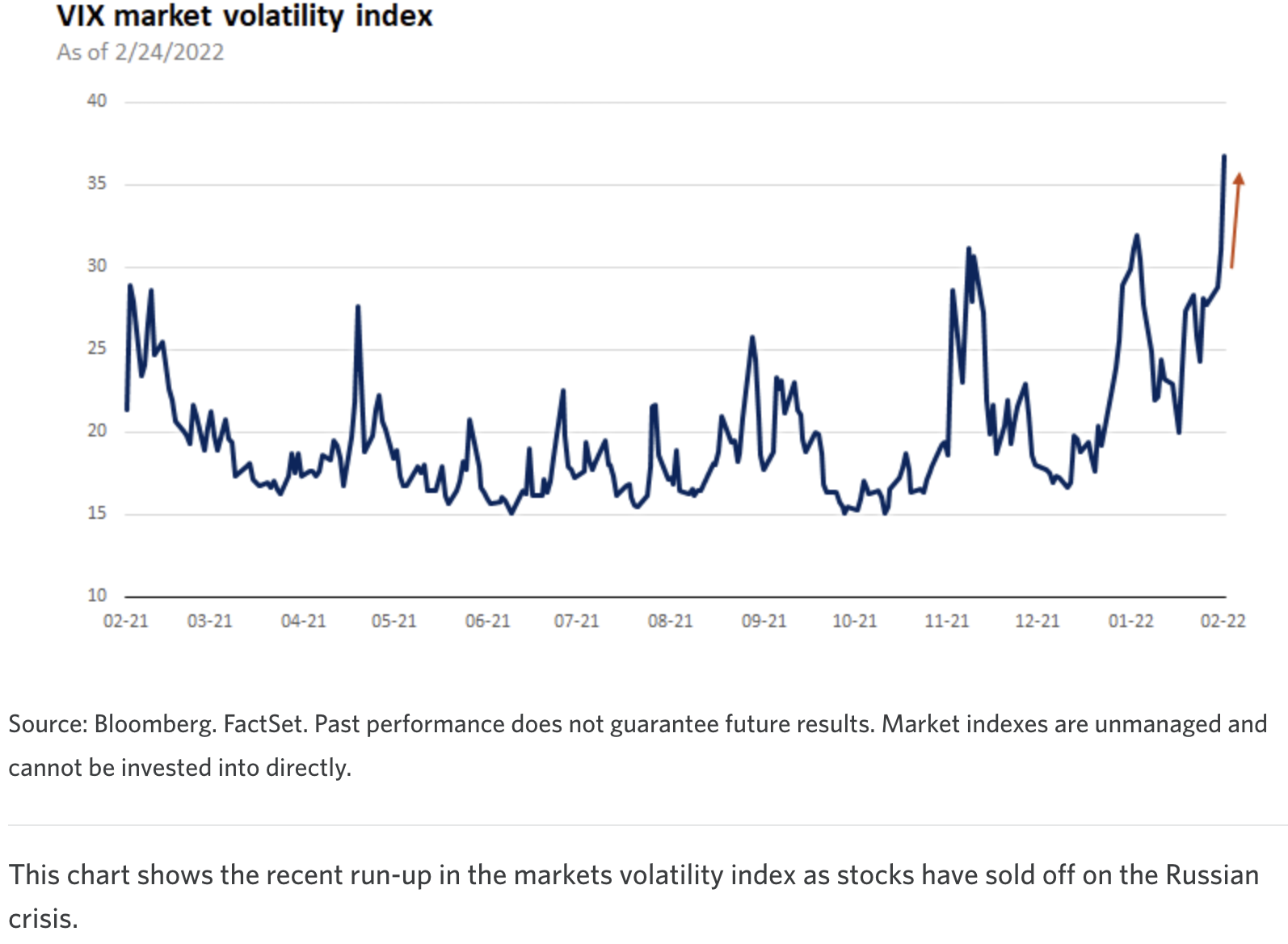

Notably, the VIX volatility index is now at its high for the year, underscoring the near-term uncertainty that markets are facing. This chart shows the recent run-up in the markets volatility index as stocks have sold off on the Russian crisis.

Geopolitical shock will drive additional volatility but shouldn't set a new course. Historically, markets tend to look past geopolitical conflicts and focus primarily on economic spillovers. Given that the situation in Ukraine has escalated beyond the level of "tensions", we don't think it's unreasonable that equity markets are reacting sharply.

However, history shows us that geopolitical events tend to be temporary, with broader economic fundamentals serving as a more sustainable market driver. Notably, the direct implications of this conflict to the U.S. economy and markets are limited, with the primary impact likely to come from potential inflationary impacts that would stem from higher commodity prices and expanding sanctions on Russian exports. These are likely to be more acute for Europe, which gets roughly 40% of its natural gas and 30% of crude oil imports from Russia.

So, while markets are likely exhibiting discomfort with the fact that the Fed will be hiking rates amid this global uncertainty, we don't expect the jump in oil prices to alter the broader path of above-trend economic growth and moderating core inflation as we progress this year.

While we still see the Fed moving forward with a rate hike in March, the probability of a 0.50% hike has come down substantially. In our view, we see scope for the Fed to move less aggressively with policy tightening this year relative to current consensus expectations, which ultimately could provide support to markets as well.

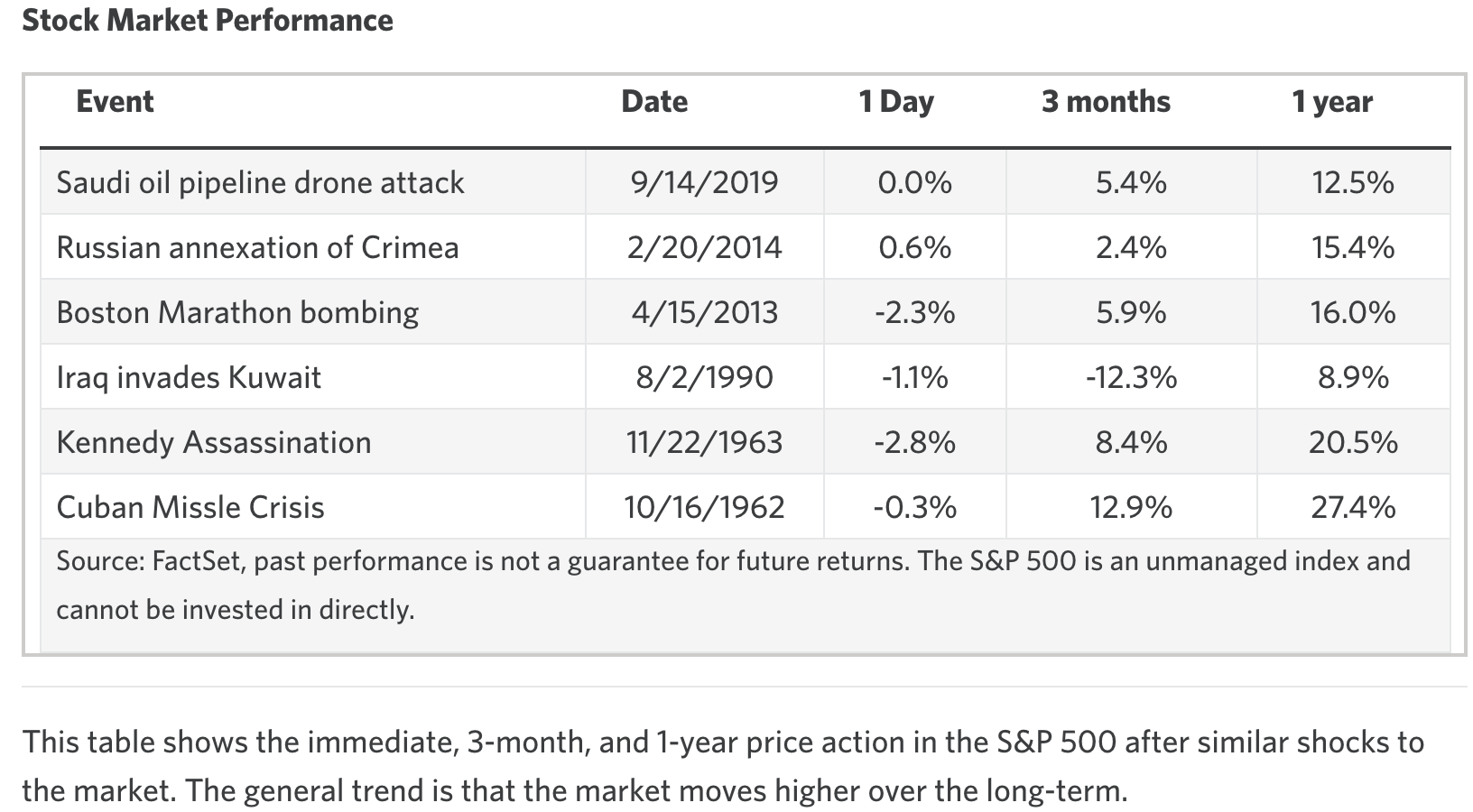

This table, above, shows the immediate, 3-month, and 1-year price action in the S&P 500 after similar shocks to the market. The general trend is that the market moves higher over the long-term. Our broader take: Markets can climb these walls of worry. The rising geopolitical tensions are certainly a headwind for markets in the near-term, and they come at a time when investors were already grappling with uncertainty around inflation and Fed rate-hike expectations.

Higher oil prices and potential supply-chain disruptions also weigh on inflation and consumer confidence. However, markets have now fallen well into correction territory, with the S&P 500 down over 10% from recent highs, perhaps now reflecting some of these headwinds.

More broadly, the S&P 500 is still up nearly 80% from the March 2020 lows1, perhaps just now giving back some of the excess valuation expansion in the post-pandemic period.

Taking a step back, we continue to see a U.S. economy that remains in the later mid-cycle of its economic expansion. This is supported by a relatively healthy consumer, above-trend economic growth, and robust corporate balance sheets and earnings growth.

While we will be watching the impacts to inflation and confidence, it is notable that the direct economic impact from Russia to the U.S. is also relatively limited, as Russia accounts for just 1% of U.S. revenues and is a minor trading partner for the U.S. (European economies have notably more exposure).

While markets are facing sizable walls of worry - both with rising geopolitical tensions and a Fed that will lay out its tightening policy in mid-March - we see the potential for stability in the weeks ahead as we get more clarity on both fronts.

Although defensive posturing makes sense in the near term, in our view market opportunities may be forming, particularly if economic and earnings growth continue to hold up well. While volatility was expected this year, investors can use these periods as opportunities to re-balance, diversify and ultimately add quality investments to portfolios at attractive prices and valuations. Action items for investors:

While market volatility is likely to remain elevated in the near term, we see the potential for stability looking further ahead as we get more clarity from both geopolitics and the Fed. While we may continue to see an investor flight to safe-haven assets in the near term, we believe buying opportunities are forming, especially if, as we believe, economic and earnings growth continue to hold up well through 2022.

We recommend using this period of volatility to rebalance, enhance diversification and ultimately add quality investments within portfolios at better valuations, as economic growth remains above trend in the year ahead.

ABOUT THE EDWARD JONES STRATEGISTS:

Mona Mahajan is responsible for developing and communicating the firm's macroeconomic and financial market views. Her background includes equity and fixed income analysis, global investment strategy and portfolio management. She regularly appears on CNBC and Bloomberg TV, and in The Wall Street Journal and Barron's. Mona has a master's in business administration from Harvard Business School and bachelor's degrees in finance and computer science from the Wharton School and the School of Engineering at the University of Pennsylvania.

Craig Fehr is a principal and the leader of investment strategy for Edward Jones. Craig is responsible for analyzing and interpreting economic trends and market conditions, along with constructing investment strategies and and asset allocation guidance designed to help investors reach their financial goals. He has been featured in Barron's, The Wall Street Journal, the Financial Times, SmartMoney magazine, MarketWatch, the Financial Post, Yahoo! Finance, Bloomberg News, Reuters, CNBC and Investment Executive TV. Craig holds a master's degree in finance from Harvard University, an MBA with an emphasis in economics from Saint Louis University and a graduate certificate in economics from Harvard.

No comments:

Post a Comment